Surrendering a life insurance policy involves terminating it before its maturity date and withdrawing the accumulated value. This process is known as policy surrender. The reasons for surrendering a policy can vary. In this article, l will guide you through the stepwise on how to surrender a LIC (Life Insurance Corporation of India) policy.

Why Surrendering Your LIC Policy Might Be Necessary

Life is unpredictable, and circumstances can change at any time. Surrendering your LIC policy may become necessary due to various reasons, including:

Financial difficulties

In times of financial difficulties, surrendering your LIC policy may be one of the options to get some cash in hand. However, surrendering policies is a challenging process. You will have to follow a process, which may take two weeks. That’s why surrendering your policy should be the last resort, and instead, have an emergency fund so that you can handle any financial difficulty easily.

Change in insurance needs

Your insurance needs may change/reduce over time, and your LIC policy may no longer align with your current insurance need. In such cases, surrendering your policy may be the best option.

Dissatisfaction with policy terms

If you are dissatisfied with the terms of your LIC policy, surrendering it may be the best option.

Better investment opportunities

It is a must to understand that the primary purpose of insurance is to protect and not to invest. In most cases, the investors hold insurance policies as they are sold as tax savings instruments.

However, there are much better tax savings investment that you can invest in for tax savings rather than insurance policies.

If you find better investment opportunities than your LIC policy, surrendering your policy and investing in those opportunities may be wise. Financial planning can help you make the right decisions in this.

Types of Life Insurance Policies

Often investors are not aware of the type of policies they hold. Here I’m sharing the type of policies so that you can get a fair idea of which type of insurance you have and which type of policies you must stay away from.

- Term Insurance: Term insurance is a pure protection plan that offers coverage for a specific term, typically ranging from 5 to 30 years. If the insured person passes away during the policy term, the death benefit is paid to the nominee. It is one of the most affordable life insurance options and provides a high coverage amount for a relatively low premium. When it comes to insurance, this is the only insurance that one must hold based on their need. These days, it’s a trend to have a one-crore cover. However, more than one crore might be required. Hence, it is better to find out how much life cover you need and buy accordingly rather than holding just one crore cover.

- Whole Life Insurance: Whole life insurance covers the insured’s entire lifetime. It includes a death benefit and an investment component known as the cash value. The policyholder pays premiums throughout their life, and upon death, the death benefit is paid to the nominee or beneficiaries.

- Endowment Policy: Endowment plans combine life insurance coverage with a savings component. These policies pay out a lump sum to the insured or their beneficiaries upon maturity (if the policyholder survives the term) or in the event of the insured’s death. It offers a guaranteed sum assured along with bonuses or returns on investment.

- Child insurance plans are part of an endowment plan designed to support a child’s financial needs. These policies provide a lump sum to the child upon maturity or in the unfortunate event of the parent’s demise during the policy term. Some child plans also offer periodic payouts for funding the child’s education at different stages. However, the reality is that at the time of taking the policy, the plan is suggested for longer tenure without considering when the money is required, and due to stringent rules on withdrawal, it creates financial stress rather than security. Hence, it’s better to keep your life cover separate and your investment separate to cover your life at a much cheaper premium in a term policy and choose the right investment product meant for investing.

- Money-Back Policy: Money-back policy provides periodic payouts during the policy term. If the insured survives the policy term, they receive the remaining sum assured along with any accrued bonuses at maturity.

- Unit-Linked Insurance Plans (ULIPs): ULIPs are market-linked insurance plans that provide life insurance coverage and investment opportunity in the equity market. A portion of the insurance premium is allocated towards life coverage, and the rest is invested in various funds (equity, debt, or balanced funds) based on the plan policyholder chooses when taking the policy. And the policyholder also gets the option to switch between the plan if they wish to. The returns are subject to market performance.

- Pension Plans/Annuity: Pension plans or annuity policies are meant to provide a regular income to the policyholder during their retirement years. It allows individuals to build a corpus during their working years, which is then utilized to generate a steady income after retirement. Consider buying this policy when you are close to retirement with a minimum 3-5 years deferment period.

When choosing a life insurance policy, it is crucial to consider the coverage amount, policy term, and premium affordability. It’s advisable to assess your requirements and consult a SEBI-registered investment adviser to select the most suitable life insurance plan.

Understanding the Surrender Value of Your LIC Policy

What is a surrender value?

Your LIC policy’s surrender value is the amount you will receive when you surrender the policy before the maturity date. It is calculated based on the number of premiums paid, the basic sum assured, and the bonuses accumulated.

Calculation of surrender value

The surrender value of your LIC or any other life insurance policy is calculated using a formula that considers the number of premiums paid, the basic sum assured, and the bonuses accumulated. The formula is as follows:

Surrender value = (Total premiums paid / Total number of premiums payable) * (Surrender value factor)

The surrender value factor is a percentage of the basic sum assured and depends on the years the policy has been in force. You can get the information directly from the insurer or the agent.

Factors that impact surrender value

The surrender value of your LIC policy is affected by various factors, including the number of premiums paid, the basic sum assured, the bonuses accumulated, and the duration of the policy.

How to Surrender LIC Policy – The Surrender Process

Step-1: Find out the surrender value

It would be best to know the surrender value first before surrendering your LIC policy. Contact your agent or customer service at 022-6827 6827 or the nearest LIC branch to determine the surrender value.

Step-2: Submitting required documents

- Request letter for surrender: In this letter, you request the LIC to take the request for the policy surrender. Here is your readymade surrender letter to download and fill in basic details like your policy number, policy name, branch name, etc, and sign.

- LIC-Policy Surrender Form: Along with the surrender request letter, you also need to submit a filled and signed LIC surrender form No.5074/3510.

- Surrender discharge form / Surrender exit interview form: In this, you let the LIC know the reason for your surrender. Here is your readymade surrender discharge form for your download. You must download, complete and sign.

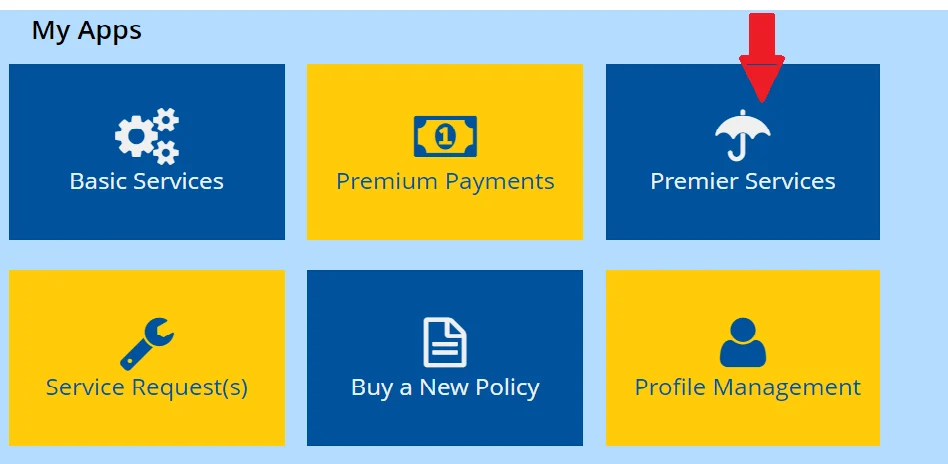

- Original LIC document: It is a must to attach your original policy bond for surrender. In case you have miss placed it, first get the duplicate policy, whether by submitting a request letter for the issue of the duplicate policy or by login into the LIC account using premier services.

To use, first, you need to opt for premium service, and then you can apply for a duplicate policy.

- 5. PAN: Attach a self-attested PAN copy.

- 6. Address Proof: Attach a self-attested address proof copy. Note: Make sure to provide the address proof of the address mentioned in the LIC policy. If you have changed your address and do not have the address proof mentioned in the policy to submit along with the surrender application, you must update your address first.

- To update your address, either you can give a physical request letter along with the self-attested new address proof to any of the LIC branches nearby or apply online by uploading self-attested new address proof via premium service.

- 7. NEFT mandate form: You must submit the filled and signed NEFT mandate form with the bank account details in which you want to receive surrender value proceeds.

- 8. Personalized cancel cheque original: Attach the original personalized cancel cheque along with all other documents mentioned above. Ensure your name on the cheque is precisely the same as your policy.

Step–3: Wait for the surrender amount

After submitting the surrender form and required documents, you must wait for the surrender value to be credited to your bank account. The process may take a few weeks to complete.

Tax Implications of Surrendering Your LIC Policy

Usually, it is said that insurance proceeds are tax-free. However, it depends upon certain conditions as per section 10(10D) of the Income Tax Act:

a) Type of policy

- Traditional Policy: If you have any traditional life insurance policy that is an endowment or money-back plan, the surrender value will be tax-free only if you have paid the premium regularly for the first two years of the policy tenure.

- ULIP Policy: If you have a ULIP policy, the surrender value will be tax-free only if you have paid the premium regularly for the first five years of the policy tenure.

b) Policy Issue Date

Apart from the type of policy, the issue date also determines the taxability of the surrender value.

- Policy issued before 31st March 2003: In this case, the surrender value is exempt from tax. Hence, tax-free.

- Policy issued between 1st April 2003 and 31st March 2012: If the premium payable in any year is within 20% of the actual sum assured, then the policy proceeds would be tax-free in the hands of the insured.

- Policy issued on or after 1st April 2012: if the premium payable in any year is within 10% of the actual sum assured, then the policy proceeds would be tax-free in the hands of the insured.

- Policy issued on or after 1st April 2013: In case the insured suffers from disease as specified by the IT act, and the insurance policy was issued on or after 1.4.2013, for them, if the premium payable in any year is within 15% of the actual sum assured, then the policy proceeds would be tax-free in the hands of the insured

Taxation of premium paid

The premiums paid towards your LIC policy are eligible for tax benefits under Section 80C of the IT Act. However, if you surrender your policy before the completion of the lock-in period, then you must reverse the tax benefits claimed on the premiums paid.

Conclusion

After considering all the options and implications, surrendering your LIC policy should be a well-thought-out decision. Before making this decision, finding the surrender value, understanding the process, and tax implications is essential. If you are still deciding whether to surrender your policy, it is advisable to consult a financial advisor. Remember, surrendering your LIC policy may have long-term financial implications and should be done carefully.

Important Articles Related to Personal Finance

- How To Invest When Sensex And Nifty All Time High?

- Maximize Your Tax Savings With Tax Harvesting Mutual Funds

- 18 Common Tax Filing Mistakes You Must Avoid FY 2022-23 (AY 2023-24

- ITR For Salaried Person: Which ITR Should I File For FY 2022-23 (AY 2023-24)?

- Tax Planning For Salaried Employees

- Unclaimed Mutual Funds In India: An Overview And Steps For Recovery

- 9 Strategies: How To Close Home Loan Early

- 5 Safe & Best Short-Term Investment Plan 2023

- Debt Mutual Funds Taxation New Rule from 1st April 2023

- All About Sukanya Samriddhi Yojana Benefits