The need to learn how to reduce loan burden smartly has increased as loans have become an integral part of an individual’s life that lenders have purposely integrated into our lives by providing attractive offers.

Whether for education, purchasing a home, starting a business, higher education, or dealing with unexpected expenses, loans often provide financial support when required. However, managing loan obligations can become a burden if not handled wisely. In this article, I will discuss smart strategies to reduce your loan burden while maintaining financial stability.

What is a Loan Trap, and the Reason Behind it?

A loan trap, often known as a debt trap, is a situation when an individual takes a loan but faces challenges repaying it. It’s not only individuals but also companies who fall into it by taking a business loan.

There are several reasons for getting into a loan trap, but here are the two major ones:

Overspending

Individuals who spend more than they earn get into a loan trap with the ease of credit card access; they often spend before earning, and that’s where the debt trap cycle starts. Then, to repay the older loan amount, they take another loan or convert the outstanding due into EMIs, and this cycle never stops.

So, the secret behind not getting into a loan trap is controlling your expenses with budgeting.

Emergency Need

Emergency needs can come in any form, including unexpected expenses, job loss, or medical conditions. Creating a minimum of 3-6 months of emergency funds for salaried professionals and business professionals of 1 year is essential. Without an emergency fund, getting into a loan trap becomes easy as you may take a personal loan or swipe a credit card and then face difficulty paying back on time.

5 Steps: How to Reduce Loan Burden Smartly

Before diving into strategies for reducing loan burdens, it’s essential to have a clear understanding of your current financial situation. Let’s understand them in steps.

Step 1: Commit to yourself with a timeline -coming out of loan burden

The first step towards reducing the loan burden is to commit to yourself; whatever it may, you will come off the loan burden and then move into the next phase of recognizing the problem that helps you set a realistic timeline for coming out of the loan burden. If you are unsure, do not hesitate to speak with people who have done it earlier or seek professional help for financial planning, where debt management is part of the process.

Step 2: Recognize the Problem

Start by analyzing the different types of outstanding loans.

Make a list of each loan (as shown in the table below), including the loan types, loan start date, interest rate, outstanding balance, and EMI payments; this will give you a comprehensive overview of your debt obligations, and then you can prioritize closing your higher interest-rate loan first.

| Types of loan | Loan Start Date | Outstanding Loan | Interest Rate | EMI (Monthly Payment) |

|---|---|---|---|---|

| Credit Card Loan | ||||

| Personal Loan | ||||

| Car Loan | ||||

| Home Loan |

Step 3: Prioritise Debt Prepayment

After you have created the list of debts as per step 2, it’s time to prioritize which loan to close first.

Remember, a newly started loan EMI always has a significant portion of the interest rate. Hence, instead of picking up high-interest-rate loans for closure, understand closing which loan is going to be more beneficial. There could be a possibility that a higher interest rate loan is almost at the end of the tenure and a lower one just newly started. Reducing new loans with lower interest rates should be prioritized in that case.

This is the most crucial stage in the debt reduction process. It will help you decide whether you should opt for home loan repayment or reduce your personal loan burden.

Tips to lower the burden of home loan EMIs

Another great way to reduce your home loan burden is to transfer your home loan balance. You can do your research and contact the bank that is providing a lower home loan interest rate, and then you can negotiate with your bank accordingly. Most likely, they will reduce your interest rate to match their competitors’, but if not, feel free to opt for a home loan balance transfer.

Step 4: Manage Your Expenses Better

As committed in step 1, whatever it may take, you will work towards reducing your loan. The process of better money management starts with understanding your expenses.

Categorize your expenses in two parts:

- Essential: All the basic expenses fall here: household expenses, school fees, travel expenses, etc

- Can be avoided or reduced: Dining out, impulse purchasing, vacation, etc. Instead of cutting small expenses, focusing on cutting down one major could be a better strategy.

Step 5: Plan Monthly Loan Pre-Payment

As you know which loan to close and, with the proper budgeting, how much additional you can save monthly, it’s time to repay your loan every month. It reminds me of a phrase: Little drops of water make a mighty ocean. A small additional pre-payment can help you become debt-free faster than you can imagine.

Pro Tip:

If you use your credit card heavily, can’t control impulse purchases with your credit card, or are already in a credit card debt trap. You must stop using your credit card immediately for further expenses. At least till the time your loan burden is sorted.

Tips To Help You Avoid Getting into Loan /Debt Traps

Live Within Your Means

Overspending is the starting point of getting into a loan trap. Living within a means and opting for a saver mindset will always help you avoid debt.

Stop Comparing with Others

A famous Hindi phrase is “har chamakti cheez sona nahi hiti,” which means not all that glitter is gold.

You might see people around you or your friends living lavishly. They might be using iPhones even if you wish to buy looking at them. But you might not be aware if they purchased it on credit card EMIs or so-called zero EMIs or were gifted by parents, etc. You can only see they live lavishly but might be in debt.

Hence, do not get attracted by looking outside, and stop comparing yourself with others.

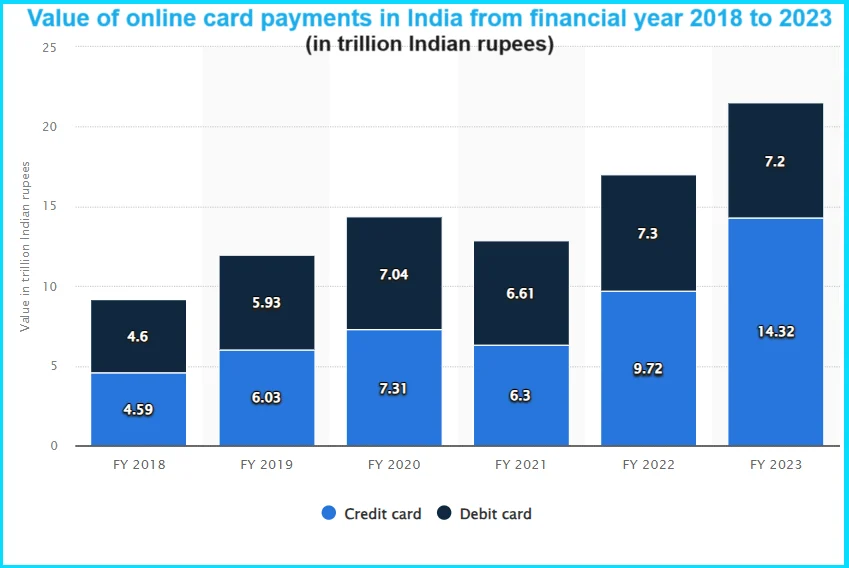

Source: Statista

Avoid Taking Multiple Loans

Multiple loans are a sure-shot strategy for getting into a loan trap. It usually starts with a personal loan followed by a home loan, then a car loan where total EMI becomes a more significant chunk of your income; this creates lots of mental pressure and financial stress, and by the time you realize it, you are already in a debt trap.

Avoid Using Multiple Credit Cards

Some individuals feel having multiple credit cards helps with better money management. You may take this with good intentions, as two cards can have two different useful offers. However, falling into a debt trap is even easier if it is not managed well. Hence, it’s better to avoid having multiple credit cards.

Conclusion

Reducing your loan burden smartly requires financial planning, discipline, and strategic decision-making. Remember that reducing and closing loans may take some time; that’s why staying patient and committed is crucial to becoming debt-free. By implementing these strategic steps, you can take control of your financial future and reduce your loan burden smartly and sustainably.

Frequently Asked Questions

Q-1: How to manage a home loan smartly?

You can manage your home loan burden smartly by following 5 steps explained in this article:

Step 1: Commit to yourself with a timeline -coming out of loan burden. Step 2: Recognize the Problem. Step 3: Prioritise Debt Prepayment. Step 4: Manage Your Expenses Better. Step 5: Plan Monthly Loan Pre-Payment

Q-2: What is the fastest way to pay off a loan?

By making an additional payment/prepayment. A small additional prepayment can help you become debt-free faster than you can imagine. You can utilize your additional savings, bonus, windfall income, etc., to prepay and close your loan faster.