Your credit score isn’t just a three-digit number—it’s your financial passport that opens doors to better interest rates, higher credit limits, and smoother loan approvals. Whether you’re planning to buy your first home, start a business, or simply want access to better financial products, understanding how to improve your credit score becomes crucial for your long-term financial health.

In India, your CIBIL score ranges from 300 to 900, and anything above 700 is generally considered a good credit score. But here is what most people don’t realize: improving your score isn’t just about paying bills—it’s about developing disciplined financial habits that compound over time.

As a fee-only financial advisor, I have seen countless individuals struggle with credit management simply because they never learned the fundamentals. The truth is, rebuilding your credit score doesn’t require expensive products or complicated strategies. It requires consistency, patience, and the right approach.

Understanding Your CIBIL Score

Let’s first examine the factors that genuinely affect your credit score before diving into ways to improve your credit. Your CIBIL report takes into account five important factors:

- Payment history accounts for 35% of your score: This is why missed payments can negatively impact your credit score so severely. Even one late payment can remain on your credit report for up to seven years, affecting your ability to establish a credit score that lenders trust.

- Credit utilization makes up 30% of your score: This is the ratio of credit you’re using compared to your available credit. Keeping your credit utilization rate below 30% is essential, though maintaining it below 10% can significantly boost your credit score faster.

- The length of your credit history contributes 15% to your score: Your credit score considers the average age of all your credit accounts, so closing an old account directly shortens the average history. This is why closing your oldest credit accounts can hurt your credit score, even if you are not using them actively.

- Credit mix accounts for 10% of your score: Having a healthy combination of revolving credit (like credit cards) and installment loans demonstrates responsible credit habits.

- New credit applications make up the remaining 10%: Too many hard inquiries within a short period can lower your credit score, as it suggests financial stress.

Behavioral Traps That Hurt Credit Scores (But People Ignore)

1. Making only minimum payments

While making minimum payments prevents late fees and protects your payment history, it keeps you in debt longer and increases total interest paid. This behavior can signal financial stress to lenders, even if your payments are technically on time.

The high balances from minimum payments also keep your credit utilisation ratios elevated, which can negatively impact your credit score over time. Aim to pay off credit card balances in full by the due date.

2. Co-signing loans without understanding the risk

When you co-sign, that debt appears on your credit report and affects your utilization ratios. If the primary borrower makes missed payments, it directly impacts your credit score. This shared responsibility can hurt your credit even when you’re not the primary user.

Before co-signing, understand that you’re equally responsible for the debt. Ensure you can afford the payments if needed, and monitor the account regularly to protect your credit profile.

Related: How to Reduce Loan Burden: 5 Step-by-Step Smart Ways to Reduce or Repay Home Loan / Personal Loan

3. Frequently closing and opening new accounts

Account churning—constantly opening and closing credit accounts—creates multiple hard inquiries and shortens your average account age. This behavior can lower your credit score and signal instability to lenders.

Instead, focus on maintaining good credit with existing accounts. Use them responsibly and consistently rather than constantly seeking new credit products.

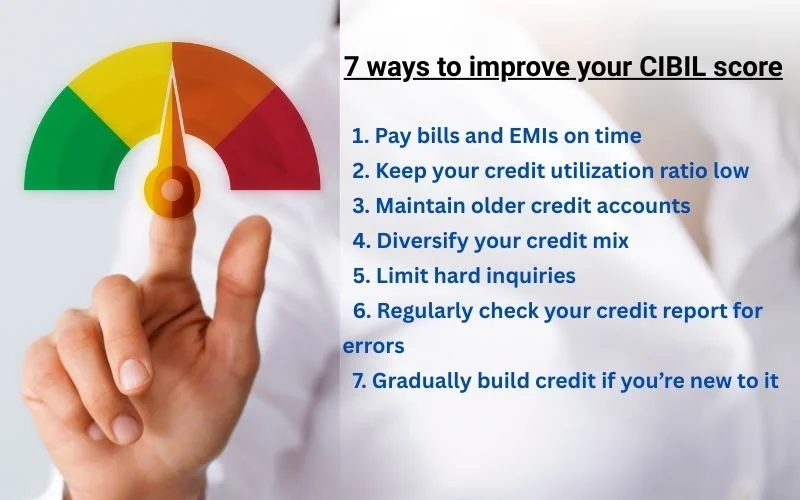

7 Proven Ways to Improve Your Credit Score

1. Pay bills and EMIs on time

This is the foundation of good credit. Your payment history is the single most important factor that can either boost your score or crash it. Paying bills on time isn’t just about credit card bills—it includes loan EMIs, utility bills, and any other financial obligation.

Setting up automatic payments ensures you never miss a due date. However, automation may become expensive if you don’t continue to review it, and that’s why I always recommend reviewing these payments monthly to maintain good credit and avoid unnecessary charges. Late payments don’t just impact your credit score; they remain on your credit report for years, making recovery more challenging.

2. Keep your credit utilization ratio low

Your credit utilization ratio is important for healthy credit. If your credit card limit is ₹1 lakh, try to keep your credit utilization ratio below ₹30,000 (30% of the credit card limit).

Keep your credit usage minimal throughout the month, not just during the payment cycle. Most people miss this strategy. Consistently keeping your utilization low shows disciplined credit behavior because credit bureaus have the right to disclose your debt at any moment.

If you consistently exceed your credit limit, you can request an increase; this automatically improves your utilization ratio and can increase your credit score over time.

3. Maintain older credit accounts

The length of credit history affects your credit profile. Your oldest account establishes how long you’ve been managing credit responsibly. Even if you don’t actively use an old credit card, keeping it open (with occasional small purchases) helps keep your credit score stable.

Closing old accounts reduces your available credit and shortens your credit history—both factors that can lower your credit score. Instead of closing, consider using these cards for small, regular expenses that you immediately pay off.

4. Diversify your credit mix

A healthy credit mix includes both revolving credit (credit cards) and installment loans (home loans, personal loans). This diversity shows lenders you can handle different types of credit responsibly, which can increase your credit rating.

However, don’t take loans just to improve your credit score. Only borrow when you genuinely need it and that you can comfortably repay. The goal is sustainable credit management, not artificial score manipulation.

5. Limit hard inquiries

Every time you apply for new credit, it results in a hard inquiry that can have impact on your credit score. Multiple inquiries within a short period can hurt your credit as it suggests you’re desperate for credit or facing financial difficulties.

Space out your applications and apply only when necessary. Research eligibility before applying to maximize chances of approval and reduce unnecessary inquiries that can remain on your report.

6. Regularly check your credit report for errors

Errors in your CIBIL report can affect your credit score, too. Common mistakes include incorrect payment history, accounts that don’t belong to you, or wrong credit card balances. These errors can significantly impact on your score if left uncorrected.

Check your credit report from all four credit bureaus in India at least once a year. If you find errors, dispute them immediately. The correction process can take to improve your score by several points once resolved.

7. Gradually build credit if you’re new to it

If you are new to credit, start small and build credit systematically. Consider a secured credit card or become an authorized user on someone else’s account to establish a credit score. The key is demonstrating positive payment history from the beginning.

For those looking to improve their scores from scratch, patience is crucial. It typically takes six months of consistent credit activity to establish a credit score, and building credit to excellent levels can take several years of disciplined behavior.

The Long-Term View: Building Credit for Future Goals

Understanding how to improve your credit score today directly impacts your future financial opportunities. A strong credit score increases your chances of getting approved for mortgages with lower interest rates, business loans with better terms, and premium credit cards with valuable benefits.

When you maintain a good credit score over time, you are not just improving numbers—you’re building financial credibility that compounds. Lenders offer their best terms to borrowers with proven track records of responsible credit management.

For major financial goals like homeownership, a difference of even 50 points in your credit score can mean thousands of rupees in interest savings over the loan term. This is why the steps to improve your credit you take today have exponential benefits tomorrow.

Strategy I Follow

Here’s a practical approach I follow and recommend to clients:

1. Consider a credit card as a debit card: Instead of waiting for bill generation, continue to clear the card balance as you use it. This positive credit behavior keeps your utilization extremely low and ensures you never spend more than you have.

2. Consider the bill date as the due date: By clearing dues before the bill generation date, your statement comes with zero balance. After that, when you swipe, you have a clear idea of the due amount. This cycle helps you avoid debt traps while maintaining excellent credit habits.

This approach does two things: it keeps your credit score high through minimal utilization, and it prevents you from accumulating debt you can’t immediately repay.

When to Seek Professional Guidance?

1. If your credit report has consistent errors

2. If you are stuck in a debt cycle and unable to improve your score despite following the basics

Position the advisor as an objective guide who can help build disciplined financial habits—not someone selling loans or products

3. If your credit report has consistent errors that you can’t resolve independently, professional help might be necessary. Sometimes, credit bureaus require additional documentation or legal intervention to correct significant mistakes.

4. If you’re stuck in a debt cycle and unable to improve your score despite following the basics, a fee-only financial advisor can help create a structured debt management plan. Unlike commission-based advisors who might push specific products, an objective guide focuses on building disciplined financial habits.

Related: Smart Debt Management Strategies to Regain Control of Your Finances

Professional guidance is particularly valuable when your score isn’t where you want it to be due to complex situations like multiple defaults, bankruptcy, or serious credit events. Recovering from more serious credit issues requires specialized strategies considering your unique circumstances.

Conclusion

Improving your credit score isn’t about quick fixes or expensive services—it’s about developing sustainable financial habits that serve you for decades. The 7 ways to improve your CIBIL score outlined above work because they address the fundamental behaviors that credit bureaus and lenders value most.

Remember, the time it takes to see significant improvement varies by individual circumstances, but most people see positive changes within three to six months of consistent effort. The key is starting today with whatever credit situation you currently have and building from there.

Your credit score plays a crucial role in your financial future, but it’s not the end goal—it’s a tool that enables bigger dreams. Focus on the behaviors that boost your score naturally: paying on time, using credit responsibly, and maintaining long-term financial discipline.

Every positive financial decision you make today contributes to keeping your credit score strong tomorrow. Start with one or two strategies, build them into habits, and gradually incorporate others. Your future self will thank you for the foundation you build today.

FAQ: How to improve your credit score?

How can I improve my credit score quickly?

Improving your credit score isn’t about quick fixes. The time it takes to see significant improvement varies by individual circumstances, but most people see positive changes within three to six months of consistent effort. You can begin by paying bills on time, including loan EMIs, utility bills, and other financial obligations.